The Federal Reserve is meeting this week, and many anticipate a cut to the Federal Funds Rate. But does that automatically mean mortgage rates will go down? Let's break it down and clear up the confusion.

The Fed Doesn't Directly Control Mortgage Rates

At the moment, all attention is focused on the Federal Reserve. Most economists anticipate that the Fed will lower the Federal Funds Rate during its mid-September meeting in an effort to prevent a possible recession.

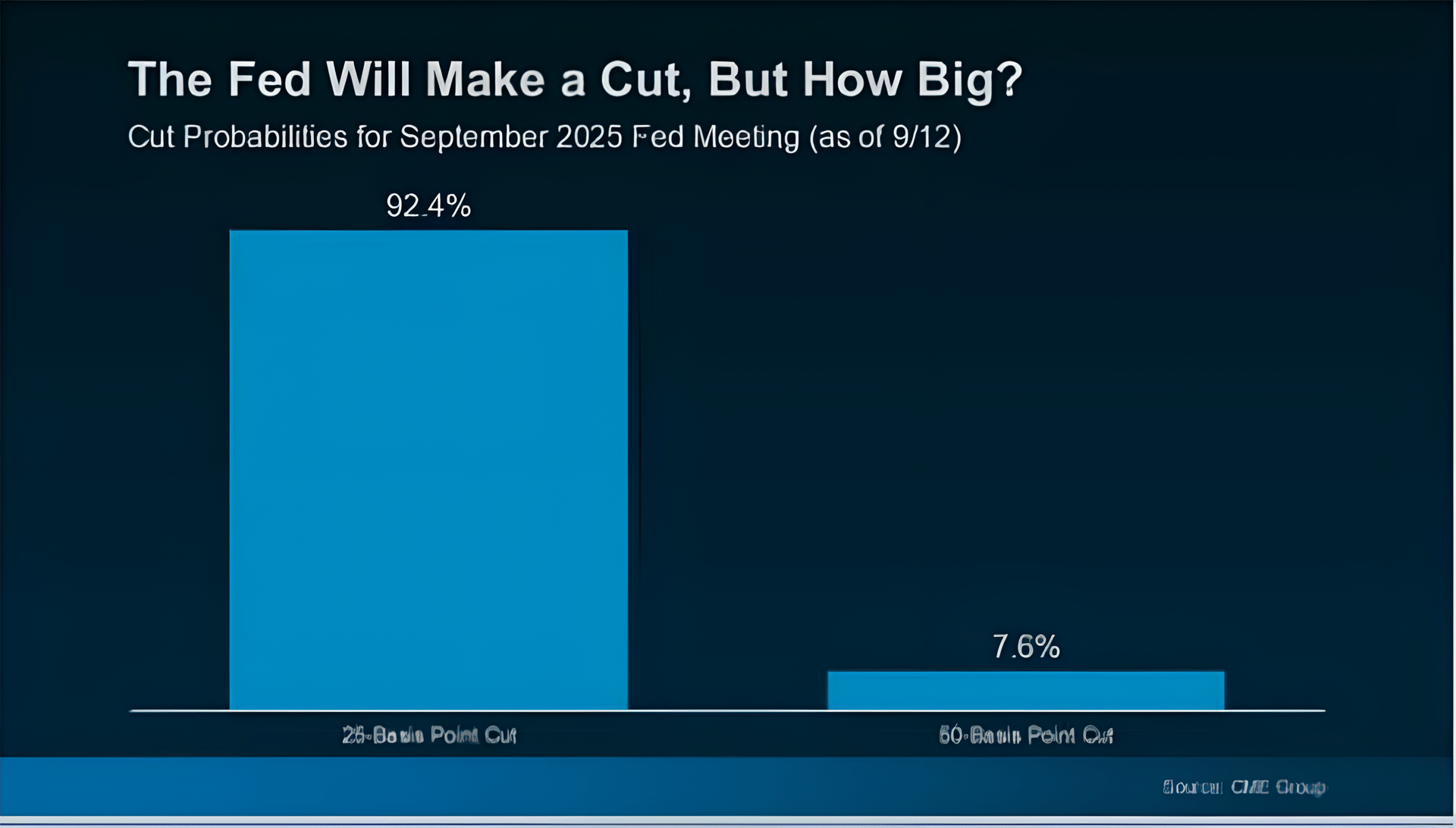

The CME FedWatch Tool shows that the market is already pricing this in, with nearly a 100% likelihood of a rate cut in September. As things currently stand, there's about a 92% chance the cut will be modest (25 basis points), and an 8% chance it will be larger (50 basis points).

So, what is the Federal Funds Rate, exactly? It's the short-term interest rate that banks charge one another for overnight loans. While it influences overall borrowing costs throughout the economy, it's not the same as mortgage rates. However, the Fed's decisions can still influence the general trend mortgage rates follow.

Why the Markets Already Expected This Rate Cut

Here's something that might surprise you: mortgage rates often move based on what the financial markets expect the Fed to do - before the Fed actually makes a move. In other words, when a rate cut

seems likely, that expectation often gets factored into mortgage rates ahead of time.

That's exactly what we saw following weaker-than-expected job reports on August 1 and September 5. In both cases, mortgage rates dipped as markets became more confident a Fed rate cut was on the horizon. And despite a slight uptick in inflation in the latest CP| report, the expectation for a cut still stands.

So, if the Fed delivers a 25-basis point cut as many expect, that move is probably already reflected in current mortgage rates-meaning we may not see much of a change.

However, if the Fed surprises with a larger 50-basis point cut, mortgage rates could fall further than they already have.

So, What's Next for Mortgage Rates?

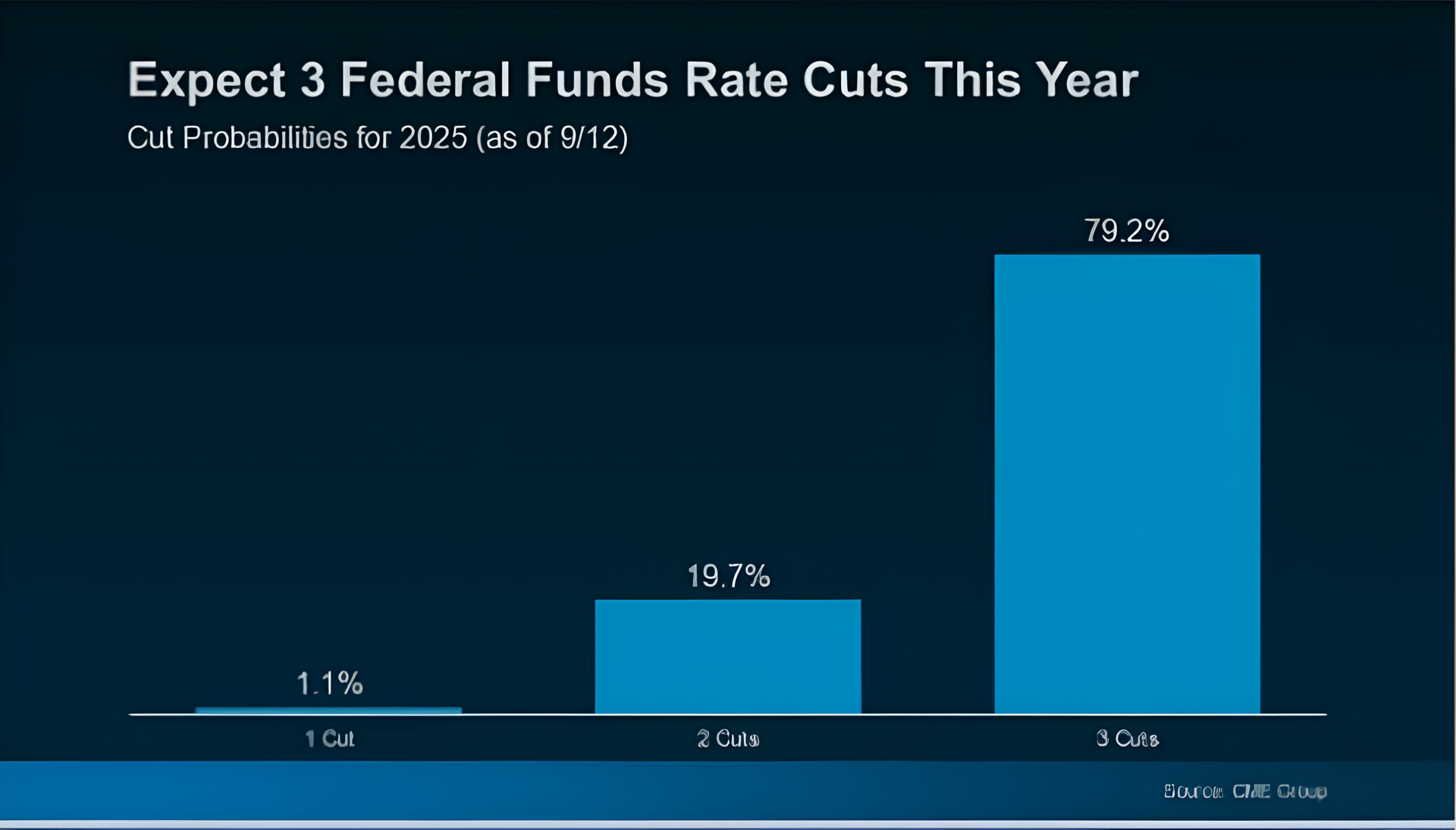

While the upcoming cut may not move the needle much, many experts expect the Fed could cut the Federal Funds Rate more than once before the end of the year. Of course, that's if the economy continues to cool (see graph below):

As Sam Williamson, Senior Economist at First American, explains:

"For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity."

If the Fed makes multiple rate cuts - or even if markets simply expect them - mortgage rates could continue to decline in the coming months.

But here's the catch: it all hinges on how the economy unfolds. Any surprise inflation numbers or unexpected economic shifts could quickly change the trajectory and market expectations.

The Takeaway

Mortgage rates probably won't plunge suddenly or move exactly in step with the Fed's decisions. However, if the Fed starts cutting rates and the markets keep anticipating more cuts, mortgage rates could gradually decline later this year and into 2026.

If you've been monitoring the housing market, now is a great time to plan your strategy. Even slight rate changes can significantly impact affordability, and knowing what to expect can help you make the best choices for your situation.